AICPA RFP Template + Winning Response Guide for CPA Firms

What happens when a single RFP response takes days of back-and-forth, scattered documents, and repeated edits? Teams often spend hours just figuring out what to include before the proposal even begins. Starting with a clear AICPA RFP template can remove much of that guesswork.

For proposal teams and vendors, unclear RFP structures create delays, missed details, and inconsistent responses. When audit or advisory opportunities appear, teams must move fast while still meeting strict documentation and evaluation requirements.

In this guide, we’ll explore what an AICPA-style RFP looks like, share a ready-to-use response template for vendors, and offer practical tips for using these templates when preparing proposals.

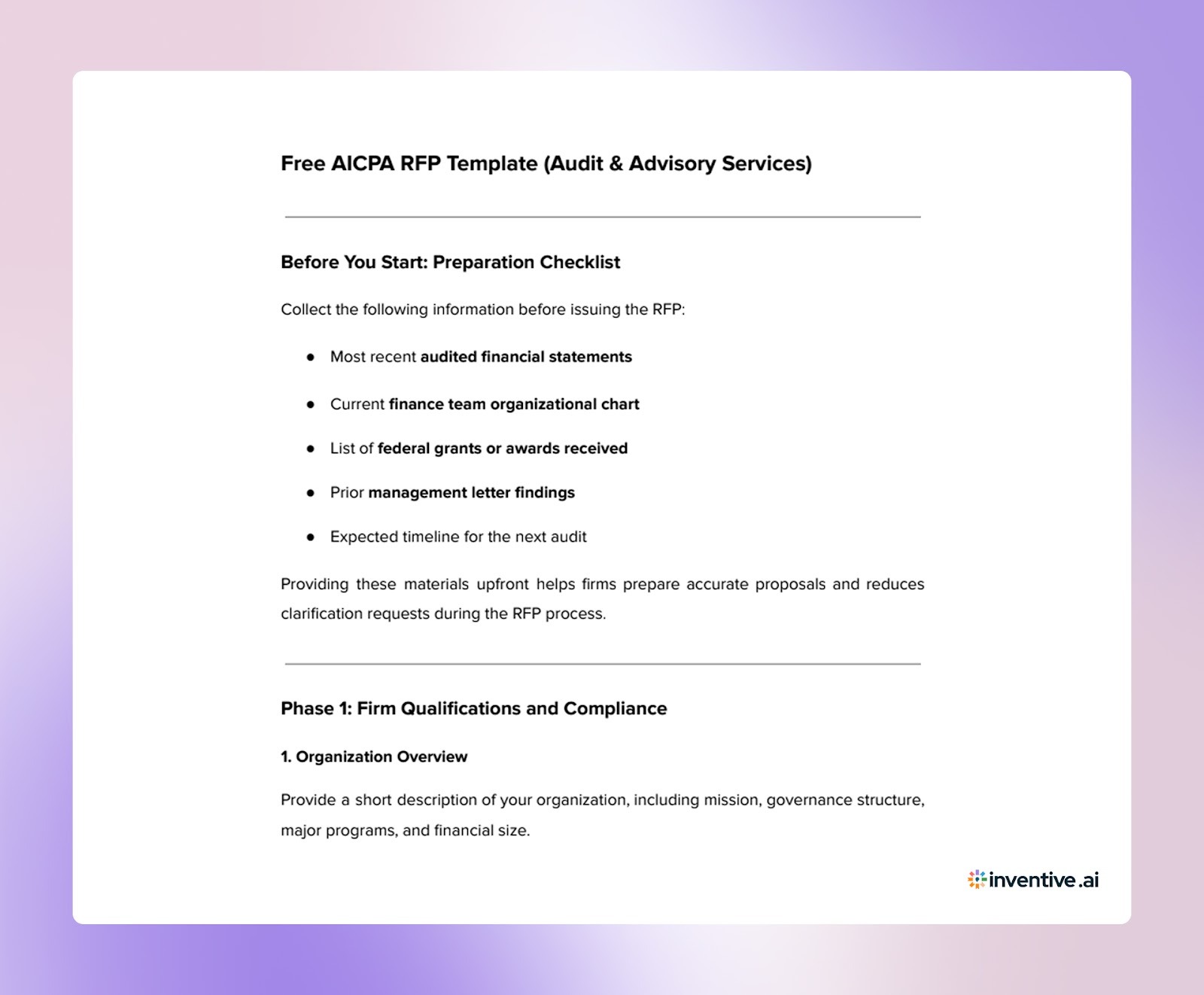

Free AICPA RFP Template for Audit & Advisory Services (for Buyers)

Organizations selecting a CPA firm typically issue a structured request aligned with AICPA professional standards. The template below reflects the sections commonly included when evaluating audit firms, covering qualifications, independence requirements, audit methodology, and pricing.

Before drafting the RFP, gather the key information vendors will need to prepare accurate proposals.

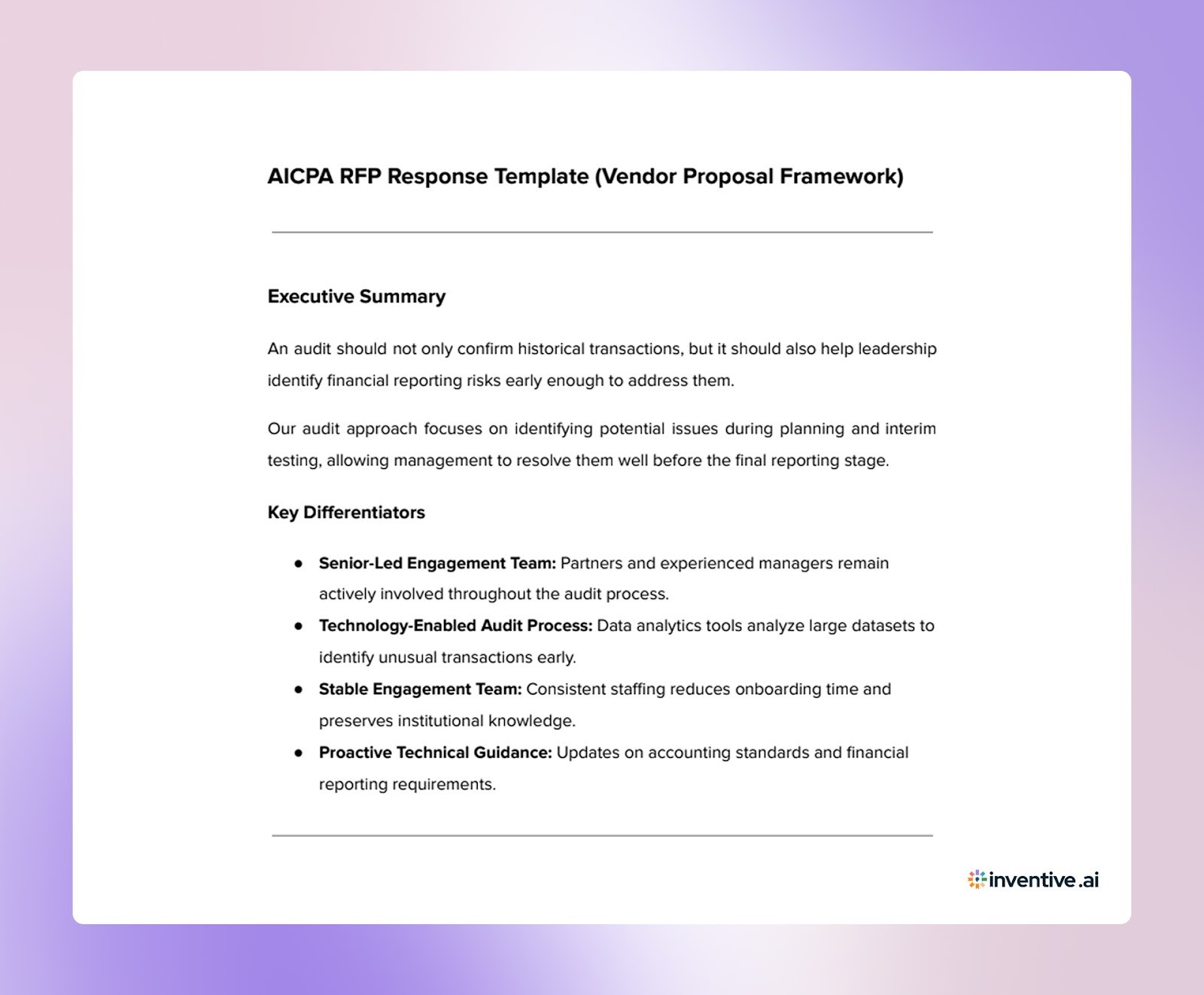

When responding to an audit request, vendors must present qualifications, methodology, and pricing in a clear format. The response template below provides a practical structure for CPA firms.

AICPA RFP Response Template for CPA Firms (For Vendors)

This template provides a structured framework for CPA firms responding to audit RFPs issued by organizations seeking independent assurance services.

Evaluation committees typically review multiple proposals and look for evidence that a firm can:

- Deliver a structured audit process

- Maintain independence and professional standards

- Minimize disruption to internal finance teams

- Provide valuable insights beyond the audit opinion

Executive Summary

An audit should not only confirm historical transactions, but it should also help leadership identify financial reporting risks early enough to address them.

Our audit approach focuses on identifying potential issues during planning and interim testing, allowing management to resolve them well before the final reporting stage.

Key Differentiators

- Senior-Led Engagement Team

Partners and experienced managers remain actively involved throughout the audit process. - Technology-Enabled Audit Process

Data analytics tools analyze large datasets to identify unusual transactions early. - Stable Engagement Team

Consistent staffing reduces onboarding time and preserves institutional knowledge. - Proactive Technical Guidance

Updates on accounting standards and financial reporting requirements.

Quick Facts for the Evaluation Committee

1. Understanding the Organization

Demonstrate your understanding of the organization’s operational and financial environment.

Key considerations may include:

- Governance structure

- Financial reporting framework

- Industry-specific regulatory requirements

- Operational factors affecting financial reporting

Showing familiarity with the organization’s environment demonstrates preparation and expertise.

2. Proposed Audit Methodology

Explain the structured approach used to perform the audit engagement.

Audit Timeline

Conducting testing earlier in the year reduces the likelihood of unexpected adjustments.

Visual Audit Workflow

Planning → Interim Testing → Year-End Fieldwork → Reporting

│ │ │ │

Weeks 1–2 Weeks 3–6 Year-End Final Report

This workflow helps finance teams understand when documentation may be requested.

Hybrid Delivery Model

Many organizations prefer a mix of remote efficiency and in-person collaboration.

Our audit approach includes:

- Secure portals for document exchange

- Virtual meetings during interim phases

- On-site participation during planning and board presentations

3. Engagement Team and Continuity

Provide details about the professionals assigned to the engagement.

Include:

- Engagement Partner

- Audit Manager

- Key audit staff members

Provide short biographies highlighting relevant experience.

Staff Continuity Commitment

Our firm strives to maintain the same core engagement team members for multi-year engagements whenever possible.

Consistent staffing improves efficiency and minimizes disruption for the client’s finance team.

4. Relevant Client Experience

Provide examples of similar engagements completed by the firm.

Examples may include:

- Organizations of comparable size or complexity

- Nonprofit or government entities

- Single Audit engagements

Short case examples help illustrate the firm’s experience with similar environments.

5. Independence and Professional Standards

Maintaining independence is fundamental to audit engagements.

Our firm maintains independence according to AICPA professional ethics standards, supported by:

- Annual independence confirmations

- Internal conflict monitoring systems

- Mandatory ethics training for all professionals

AICPA Peer Review Results

Our most recent AICPA Peer Review (2025) resulted in:

Pass (No Letter of Comment)

In simple terms, this represents the highest level of quality assurance available through peer review, confirming that our audit practices meet professional standards verified by other CPA firms.

6. Data Security and Privacy Controls

Audit engagements involve the exchange of sensitive financial information.

Our firm protects client data through:

- Secure document portals

- Encryption protocols

- Internal cybersecurity policies

Many firms also maintain SOC 2 or comparable security certifications.

7. Audit Technology and Analytics

Technology plays a key role in modern audit engagements.

Examples of tools firms may use include:

- Data extraction from accounting systems

- Analytics platforms such as CaseWare or MindBridge

- Automated anomaly detection tools

These technologies allow auditors to analyze complete datasets rather than relying solely on traditional sampling.

8. Communication With Management and Governance

Explain how the audit team communicates with leadership during the engagement.

Typical communication includes:

- Regular status updates

- Discussion of significant audit findings

- Delivery of the management letter

Clear communication helps leadership understand audit results and the recommended improvements.

9. Transition and Onboarding Plan

If the organization is changing auditors, describe how the transition will be managed.

Day-1 to Day-30 Transition Plan

Week 1

- Introduce the engagement team

- Coordinate with the predecessor auditor

Week 2

- Review prior workpapers

- Establish document request schedule

Week 3

- Conduct planning meetings

- Begin internal control walkthroughs

Week 4

- Finalize audit timeline and document requests

Our team typically takes the lead in coordinating with the prior auditor, minimizing the workload placed on the client’s finance team.

10. Single Audit Expertise (If Applicable)

Organizations receiving federal funding may require a Single Audit under Uniform Guidance.

Our approach includes:

- Compliance testing for federal programs

- Internal control reviews related to grant administration

- Preparation of required federal reporting

Early identification of compliance risks helps organizations avoid findings that could affect future funding.

11. Project Management and Document Portal

Efficient document exchange is critical during the audit process.

Our firm typically uses a secure document portal and project management system that allows clients to:

- Upload the requested documentation

- Track outstanding requests

- Communicate with the audit team

These systems help reduce email chains and improve visibility into audit progress.

12. Pricing Structure

Provide a clear pricing proposal for the engagement.

This may include:

- Fixed fee for the first year

- Estimated hours by staff level

- Expected out-of-pocket expenses

Scope Change Transparency

Additional work may occur when circumstances change, such as:

- Discovery of material financial misstatements

- New regulatory requirements

- Addition of federal grant funding requires a Single Audit

When scope changes occur, they are discussed with management before additional work begins.

13. Value Beyond the Audit

Audit engagements often generate insights useful to leadership.

Management Letter

Our firm provides a Management Letter identifying internal control observations.

Recommendations are typically prioritized as:

- High Impact

- Medium Impact

- Low Impact

This helps leadership focus on improvements that provide the greatest benefit.

Benchmarking Insights

Some firms provide benchmarking reports comparing financial ratios against industry averages.

These insights may include:

- Program expense ratios

- Administrative cost comparisons

- Financial sustainability indicators

14. Year-Round Technical Guidance

Organizations may benefit from ongoing access to accounting expertise.

Examples include:

- Updates on new accounting standards

- Informational briefings for finance teams

- Technical discussions regarding financial reporting issues

15. Firm Culture and DEI Commitment

Some organizations request information about firm culture and workforce diversity.

This section may describe:

- Diversity and inclusion initiatives

- Professional development programs

- Community engagement activities

Even with a strong template, preparing a proposal still requires careful coordination between subject matter experts, proposal teams, and leadership.

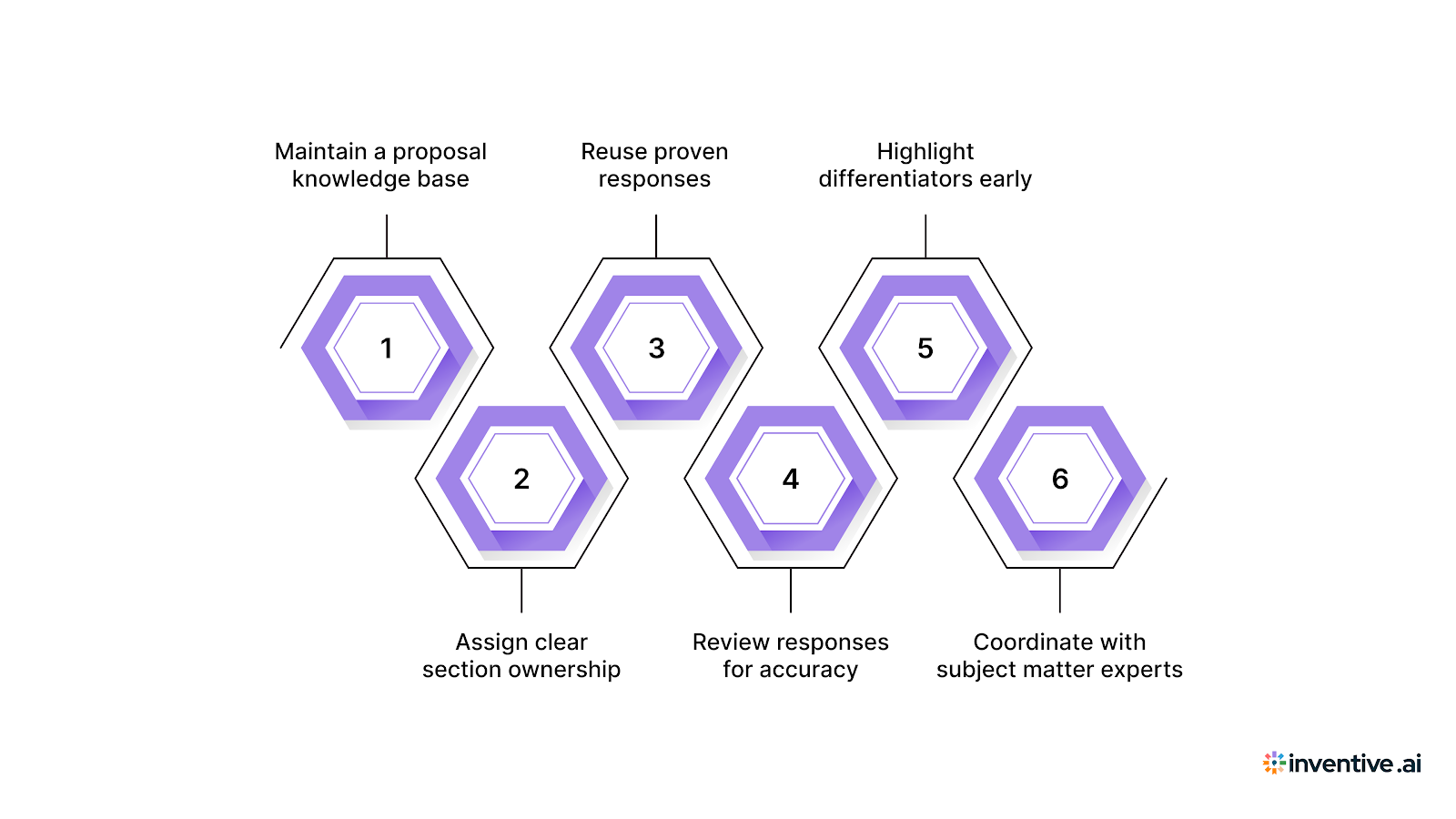

Six Tips for Writing a Winning AICPA RFP Response

Writing an RFP response often requires input from proposal managers, finance leaders, subject matter experts, and sales teams. Without a clear process, teams can spend hours searching for past answers or updating outdated content.

To keep responses clear and consistent, teams can follow a few practical habits when preparing proposals:

- Maintain a proposal knowledge base: Store past RFP answers, audit methodology descriptions, and compliance responses in a shared location so teams can reference them quickly when new proposals arrive.

- Assign clear section ownership: Define who owns each part of the response, such as technical methodology, security controls, pricing, and client references, to avoid duplicate work and conflicting answers.

- Reuse proven responses: Many RFP questions repeat across proposals. Keeping approved answers ready allows teams to respond faster while maintaining consistent messaging.

- Review responses for accuracy: Accounting standards, audit tools, and service offerings change over time. Periodically review stored responses so that outdated information does not appear in new proposals.

- Highlight differentiators early: Selection committees often review multiple submissions. Placing key strengths, such as industry experience or technology tools, near the beginning helps reviewers identify value quickly.

- Coordinate with subject matter experts: Technical sections such as compliance, data security, or Single Audit requirements may require input from specialists. Involving them early helps prevent last-minute edits.

How Inventive AI Helps Teams Respond to AICPA RFPs Faster?

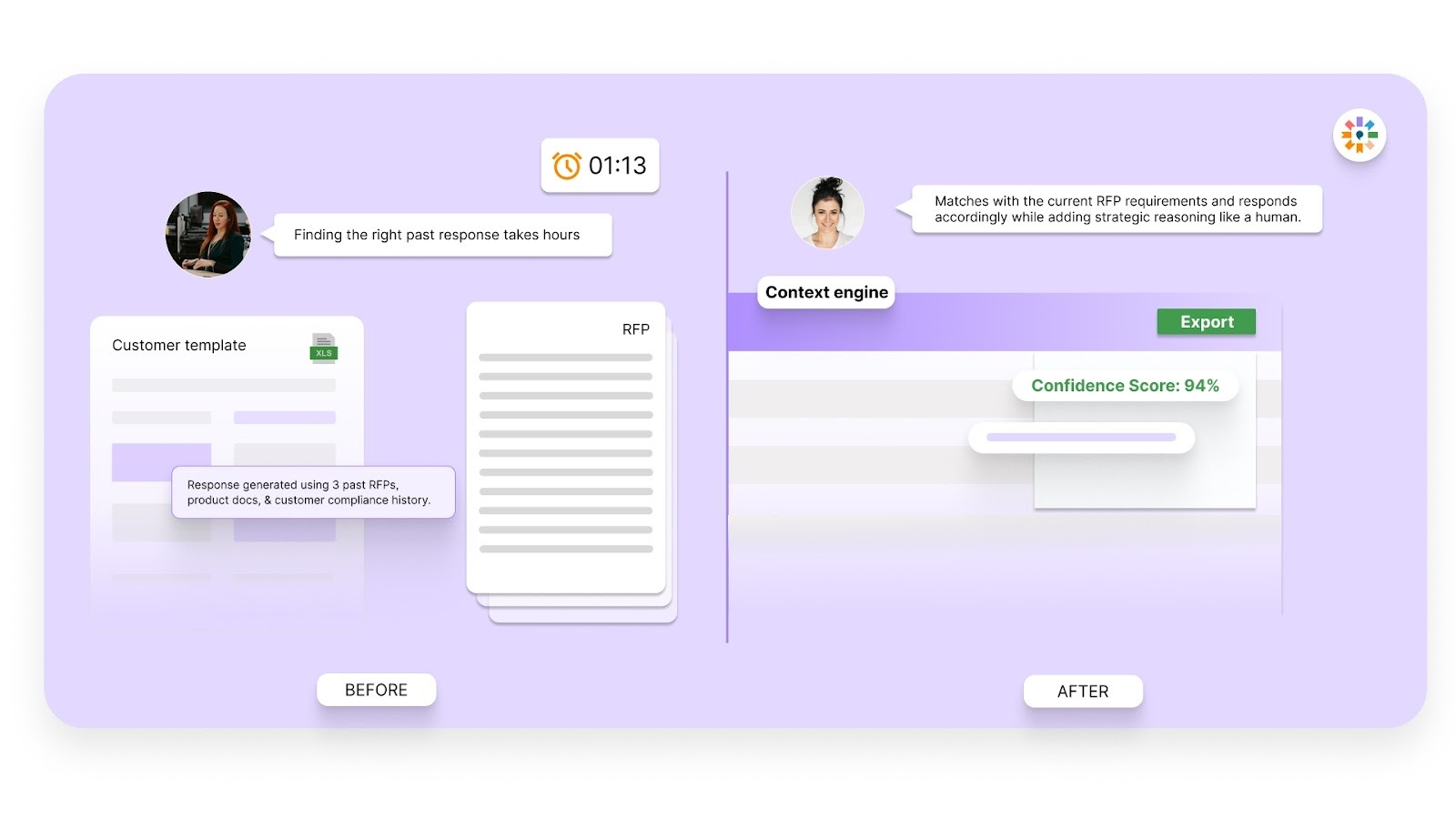

Preparing RFP responses often requires teams to search through past proposals, review multiple knowledge sources, and verify that responses remain accurate. This process can take significant time, especially when responses must meet strict compliance or audit standards.

Inventive AI supports proposal teams in producing stronger responses by analyzing the full RFP context and keeping answers consistent and up to date.

Context Engine for accurate responses

Inventive AI analyzes the full RFP context rather than matching isolated questions. Its multi-layer reasoning reviews surrounding sections, previous answers, and knowledge sources to generate responses that reflect the intent of the question and read like they were written by a subject matter expert.

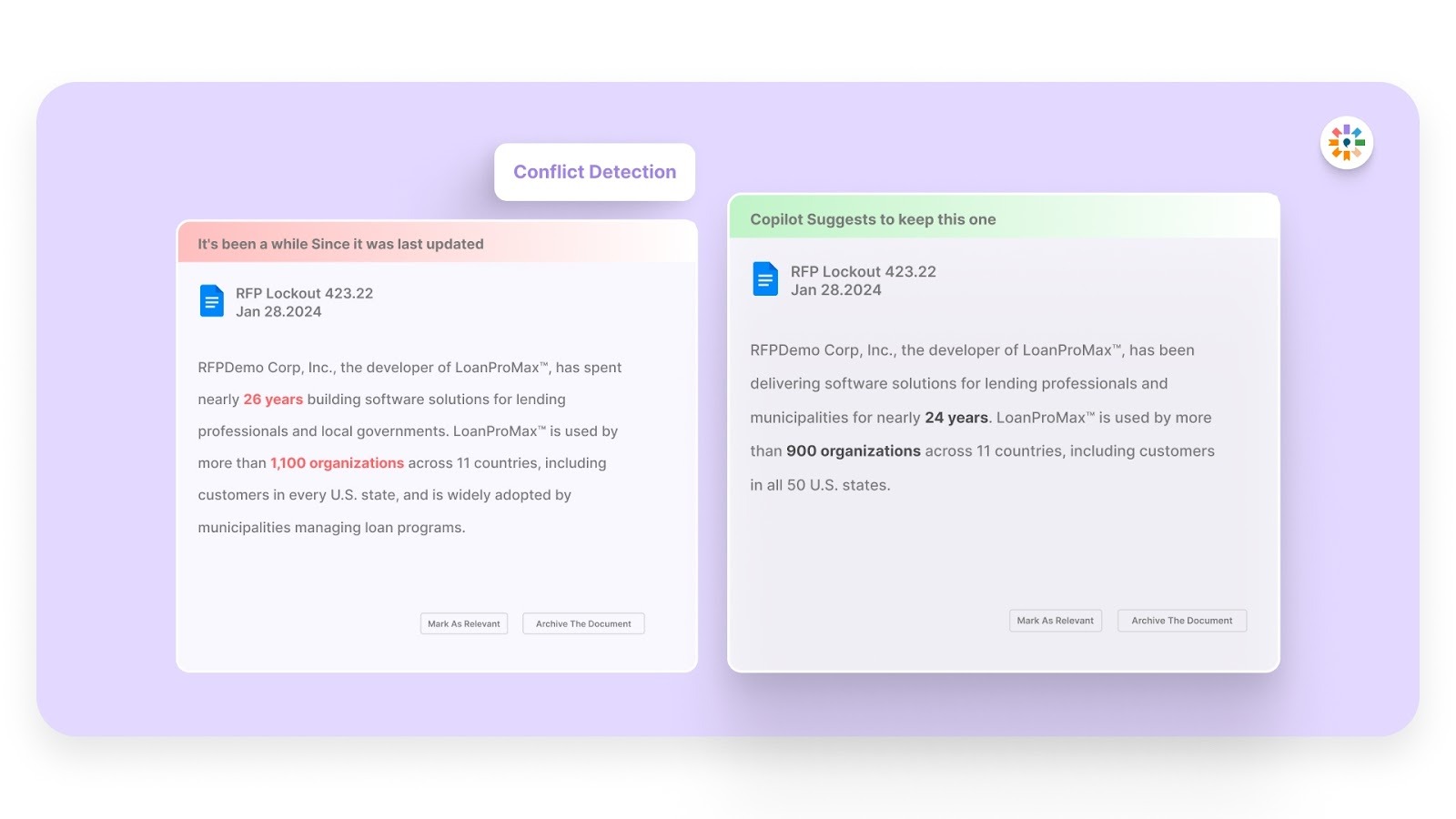

Conflict detection across responses

Inventive AI automatically scans your response library and identifies conflicting statements across documents. When contradictions appear, the platform flags them instantly so teams can correct issues before submitting proposals and avoid sending inconsistent information to buyers.

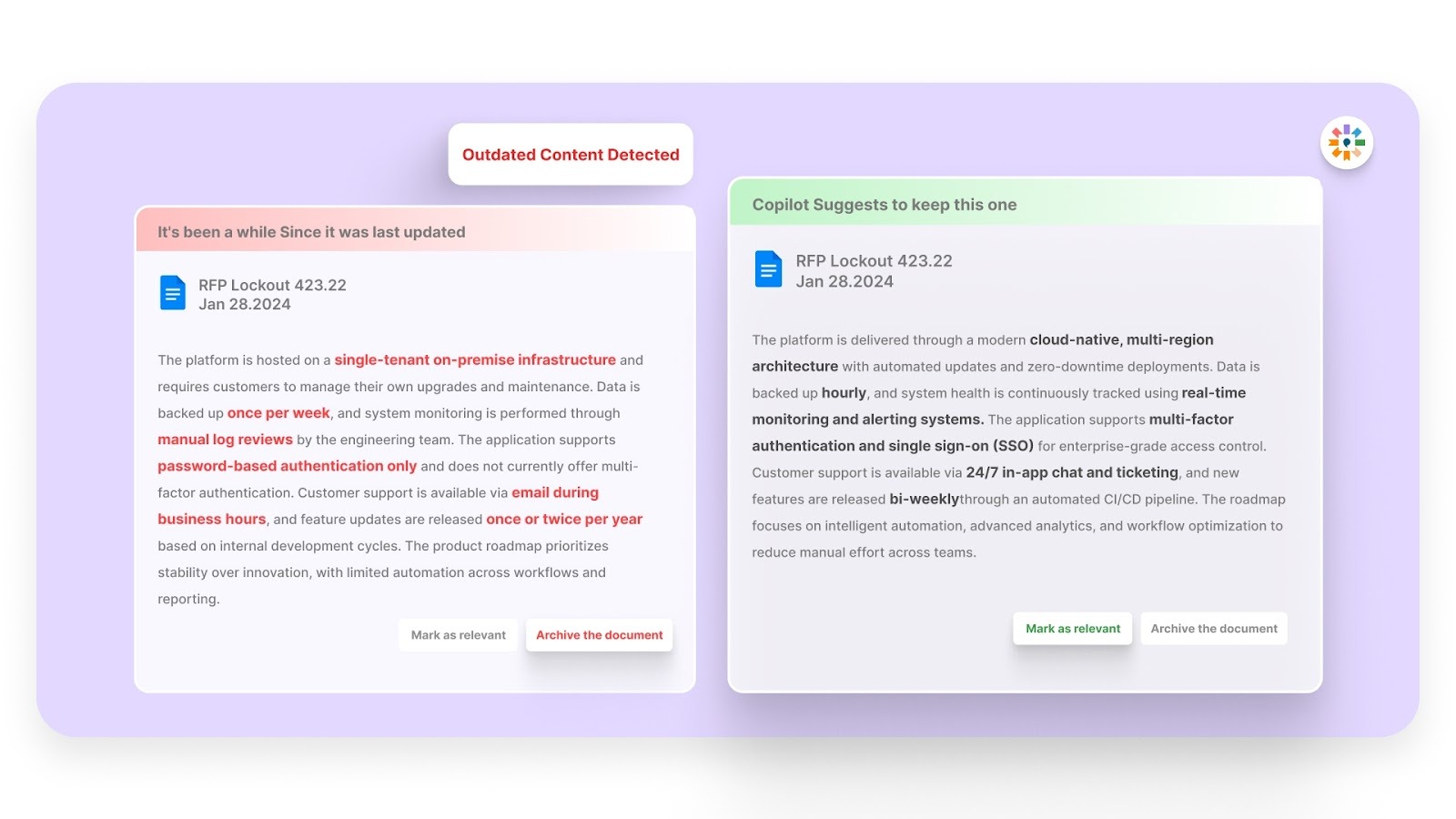

Outdated content detection

Many teams maintain large repositories of past answers that may no longer reflect current policies, standards, or service offerings. Inventive AI identifies outdated or non-compliant responses so teams can update them before reuse, reducing the time spent reviewing content manually.

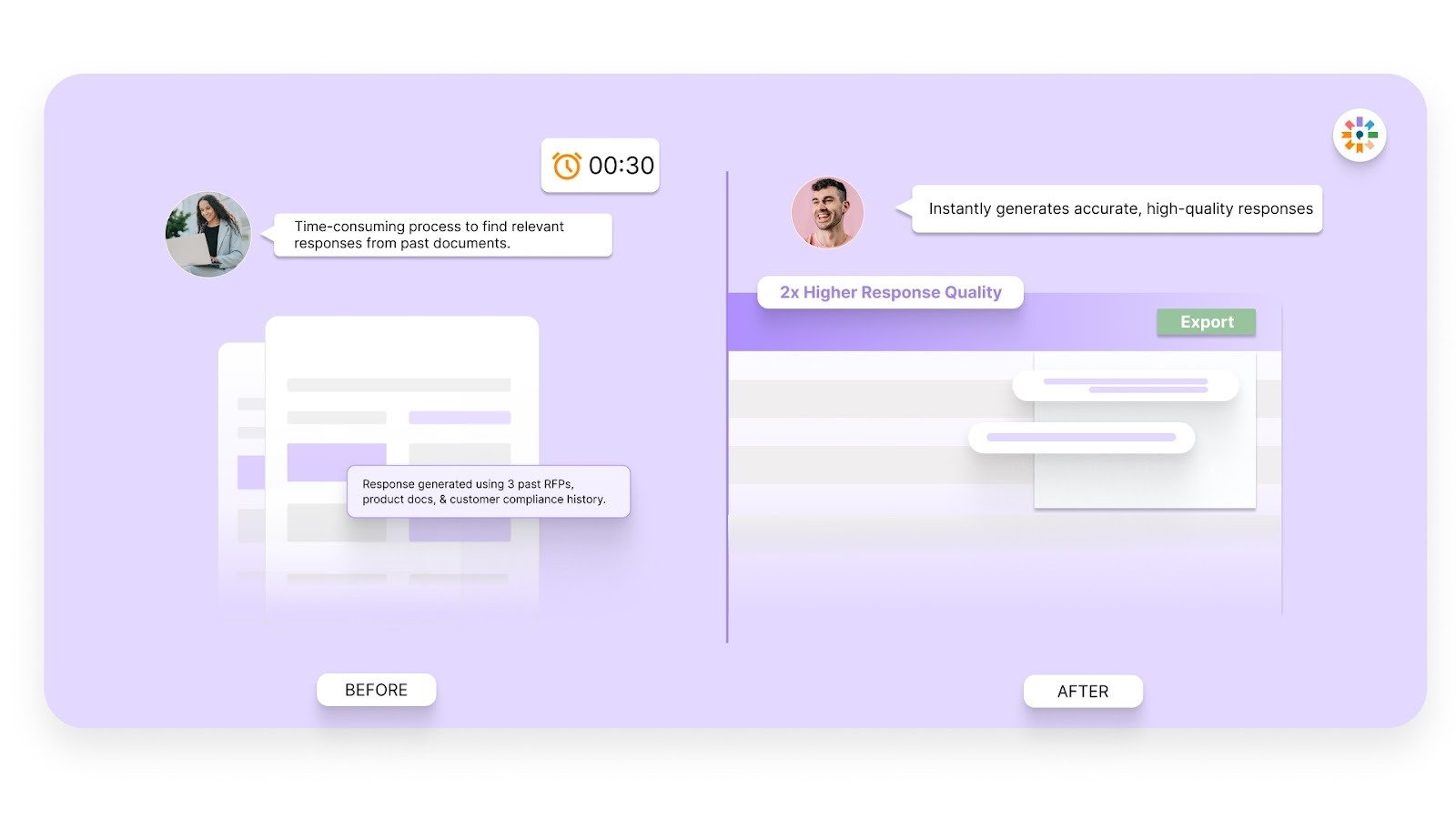

2x Higher-quality responses with multi-agent AI

Inventive AI’s multi-agent system evaluates the purpose behind each question and generates responses designed for clarity, completeness, and accuracy. This helps proposal teams produce answers that address buyer intent while maintaining consistency across the entire proposal.

Simple and easy-to-use interface

Inventive AI offers an intuitive interface that allows proposal, sales, and solutions teams to start using the platform quickly. With high adoption across current customers and strong usability ratings on G2, teams can begin generating responses without complex setup or training.

FAQs

1. Who typically issues an AICPA-style RFP?

Organizations that require independent audit or advisory services often issue these requests. This may include nonprofits, private companies, public sector entities, and organizations that must meet board or regulatory reporting requirements.

2. When should an organization issue an audit RFP?

Many organizations issue an audit request when their current engagement term is ending, when leadership changes occur, or when the board requests a review of audit providers. Some organizations also run an RFP every few years as part of governance policies.

3. How long does an audit RFP process usually take?

The timeline can vary depending on the size of the organization and the number of vendors invited to respond. Many audit selections follow a process that spans several weeks, including the RFP release, vendor questions, proposal submission, and evaluation.

4. What documents should vendors review before preparing an RFP response?

Vendors often review publicly available financial statements, prior audit reports, and any background materials included with the request. These documents help the firm understand the organization’s reporting environment and prepare a more accurate proposal.

5. How do evaluation committees compare audit proposals?

Committees often review proposals using a scoring framework that considers factors such as firm experience, proposed team members, audit approach, and pricing. This structured review helps decision makers evaluate multiple proposals consistently.

90% Faster RFPs. 50% More Wins. Watch a 2-Minute Demo.

Gaurav Nemade

After witnessing the gap between generic AI models and the high precision required for business proposals, Gaurav co-founded Inventive AI to bring true intelligence to the RFP process. An IIT Roorkee graduate with deep expertise in building Large Language Models (LLMs), he focuses on ensuring product teams spend less time on repetitive technical questionnaires and more time on innovation.

.avif)

Mukund Kumar

Understanding that sales leaders struggle to cut through the hype of generic AI, Mukund focuses on connecting enterprises with the specialized RFP automation they actually need at Inventive AI. An IIT Jodhpur graduate with 3+ years in growth marketing, he uses data-driven strategies to help teams discover the solution to their proposal headaches and scale their revenue operations.