Insurance RFPs Simplified: Strategies for Smarter Proposals and Responses

This guide explains what an insurance RFP is, how the two-tier broker–carrier model works, and how organizations issue, evaluate, and respond to insurance RFPs.

Securing insurance coverage requires careful evaluation of risk, pricing, service capability, and long-term claims support. Insurance RFPs provide a structured way for organizations to assess brokers and coverage options using consistent requirements and evaluation criteria, reducing ambiguity in high-stakes insurance decisions.

According to McKinsey’s Global Insurance Report 2025, commercial property and casualty insurance premiums grew by an average of 8 percent annually over the past five years, with industry combined ratios improving to approximately 91 percent in 2023. This environment increases scrutiny on coverage structure, exclusions, claims handling, and broker performance, making structured RFP processes more critical than informal renewals or ad-hoc comparisons.

This guide explains what an insurance RFP is, how the two-tier broker–carrier model works, and how organizations issue, evaluate, and respond to insurance RFPs. It also examines common execution gaps and how teams are improving response consistency and efficiency as RFP volumes increase.

Key Takeaways

- Insurance RFPs are a two-stage decision process where broker selection directly shapes carrier access, coverage structure, underwriting outcomes, and long-term claims performance.

- The quality of insurance proposals is determined before responses arrive, based on how clearly risk data, scope, timelines, and evaluation criteria are defined at the issuing stage.

- High-performing insurance RFPs rely on structured components, including background data, scope clarity, targeted questionnaires, and weighted evaluation criteria, to make proposals comparable and defensible.

- Manual insurance RFP responses break down under volume due to repeated drafting, fragmented information, formatting work, and review-heavy workflows that do not scale.

- AI-based RFP automation replaces manual assembly with structured, approved response generation, enabling teams to submit consistent, review-ready insurance proposals at scale without increasing effort.

- Inventive AI supports insurance RFP responses by generating structured, review-ready answers from approved content, reducing manual drafting and rework while maintaining consistency across submissions.

What's an RFP for Insurance?

An RFP for insurance is a formal document issued by an organization seeking insurance coverage. It’s designed to get detailed proposals from prospective brokers, enabling a structured comparison of their qualifications, services, and value propositions.

Typically, an RFP includes background information about the organization, its insurance needs, and specific questions or requirements that respondents must address.

How Insurance RFPs Work? The Two-Tier Model

Unlike most industries, insurance RFPs typically follow a two-tier structure.

In the first stage, organizations issue an RFP to select an insurance broker. This broker is responsible for understanding the organization’s risk profile, structuring coverage requirements, and managing market access.

In the second stage, the selected broker issues RFPs to insurance carriers on the organization’s behalf. Carriers then propose coverage terms, pricing, exclusions, and underwriting conditions.

This model allows organizations to:

- Leverage broker expertise and insurer relationships

- Access a wider carrier market without managing multiple negotiations

- Ensure coverage options are structured consistently for fair comparison

Understanding this distinction is essential, as broker selection directly influences carrier outcomes.

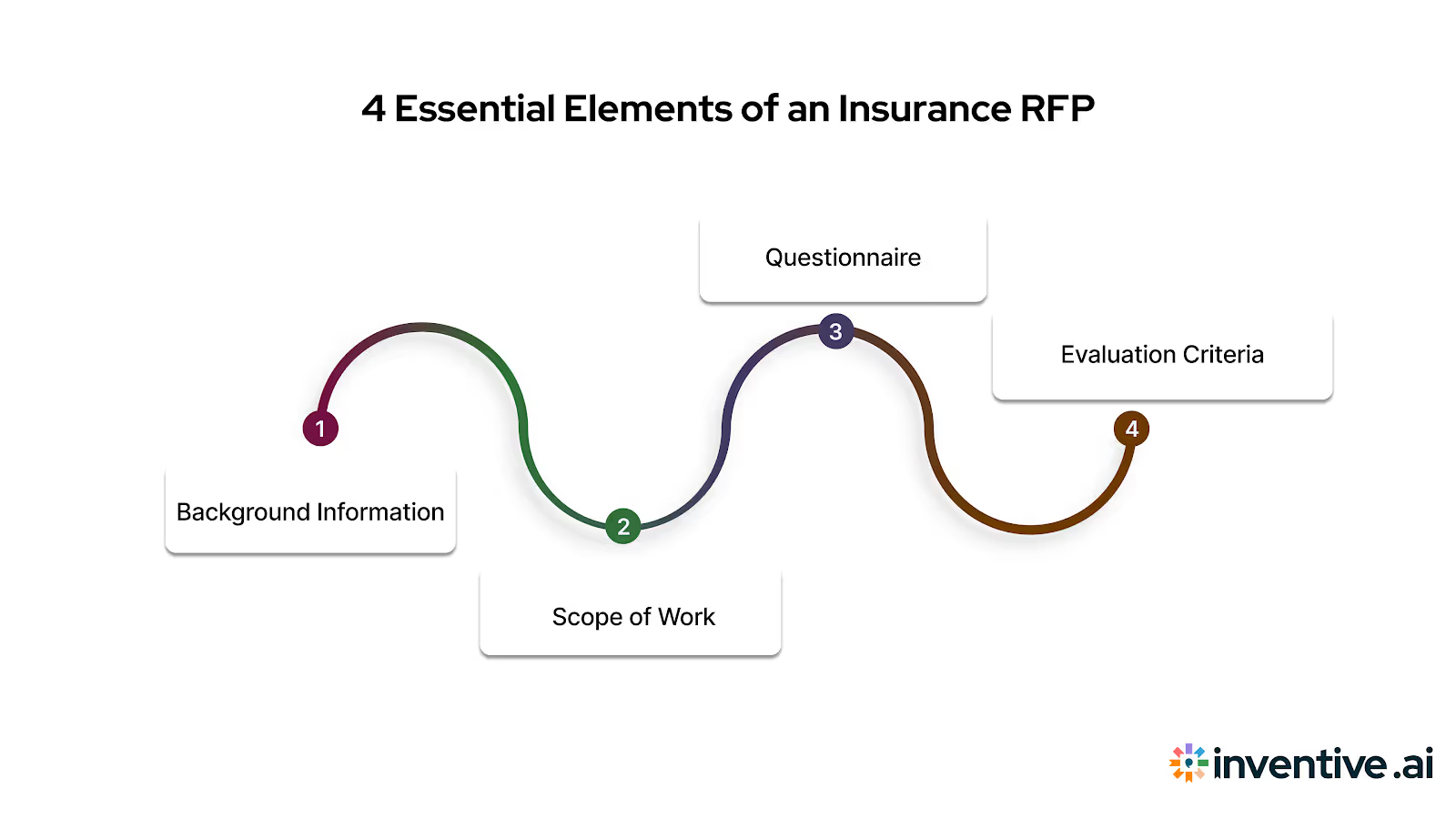

4 Key Components of an Insurance RFP

An insurance RFP must provide enough structure and clarity for brokers or carriers to assess risk accurately, price coverage correctly, and propose relevant services.

Each section of the RFP plays a specific role in eliminating ambiguity, standardizing responses, and enabling fair comparison across proposals.

While the exact structure may vary by organization and coverage type, high-performing insurance RFPs consistently include the following core components.

1. Background Information

Providing detailed context about your organization sets the stage for a well-tailored response from potential brokers. Key elements to include are:

- Organization Overview: Describe your company’s size, industry, and geographic locations. For instance, a manufacturing firm with 500 employees across three states would have different needs than a tech startup with a remote workforce.

- Current Coverage Details: Outline existing insurance policies, including carriers, coverage limits, and expiration dates.

- Goals and Challenges: Share your objectives (e.g., better rates, enhanced coverage) and any pain points (e.g., compliance issues or service gaps).

2. Scope of Work

This section details the services and expertise you require from the broker. Be as specific as possible to ensure responses address your unique needs.

Key Areas to Include:

Service Requirements:

- Consulting on insurance coverage options

- Claims management and support

- Regulatory compliance assistance

- Risk management services

Technology Expectations:

- Integration with existing HR or finance systems

- Reporting and analytics tools

Communication and Support:

- Frequency of updates and meetings

- Dedicated account managers

3. Questionnaire

The questionnaire is a critical part of your RFP, enabling you to assess potential brokers’ qualifications and approach. Tailor questions to extract meaningful insights.

Suggested Questions:

General Information

- Firm’s History: Founded in [Year], with a track record of delivering tailored insurance solutions to businesses across various industries.

- Mission and Values: Dedicated to providing comprehensive coverage, reducing risk, and building long-term client relationships based on trust, innovation, and transparency.

- Differentiation: Specialized in risk assessment, leveraging proprietary tools, strong insurer partnerships, and deep expertise in complex policy structures.

Expertise and Experience

- Industry-Specific Expertise: Currently serve [specific number] of clients in [specific industry], handling sector-specific risks like professional liability, workers' compensation, or cyber insurance.

- Case Studies: Successfully reduced liability premiums for a mid-sized tech company by 20% while enhancing coverage. Reference available upon request.

Services and Support

- Policy Management Tools: Provide an online platform for real-time policy tracking, renewal alerts, claims submission, and centralized document access.

- Compliance Support: Conducts regular compliance audits to ensure policies align with industry regulations, like OSHA, HIPAA, or state-specific insurance mandates.

Cost and Transparency

- Fee Structure: Transparent commission-based or flat-fee model, with all additional costs outlined upfront (e.g., endorsements or amendments).

- Competitive Pricing: Conducts annual market evaluations and negotiates aggressively with insurers to ensure clients receive optimal pricing and coverage terms.

Example

4. Evaluation Criteria

Establishing clear criteria ensures you can objectively compare proposals. Define metrics based on organizational priorities, and assign weight to each criterion to reflect its importance.

Key metrics to consider:

Cost Effectiveness:

- Total premium costs for policies tailored to your needs.

- Transparency in fee structure, including commission, service charges, and any additional costs for endorsements or amendments.

Service Quality:

- Breadth of services, such as claims assistance, risk management, and coverage optimization.

- Depth of support, including personalized consultations and proactive policy reviews.

Technology and Tools:

- Availability of user-friendly platforms for policy management, claims tracking, and renewal alerts.

- Access to advanced analytics tools for risk assessment and cost optimization.

Industry Expertise:

- Demonstrated experience in your industry, supported by case studies and references.

- A record of tailoring policies to address specific risks and challenges faced by similar clients.

Compliance and Risk Management:

- Proven track record of managing regulatory challenges and ensuring compliance with industry standards (e.g., OSHA, HIPAA).

- Support for risk mitigation strategies, including regular audits and training resources.

Claims Settlement Ratio:

- High percentage of claims settled compared to total claims filed, indicating efficiency and reliability in claims handling.

- Average time taken to resolve claims, ensuring swift payouts and minimized disruptions.

Premium-to-Payout Ratio:

- Assessment of the ratio between premiums collected and claims paid out, showcasing value for clients.

Coverage:

- Comprehensive policy options with flexibility to address unique business risks.

- Inclusion of critical insurance terms such as limits, exclusions, sub-limits, and endorsements to ensure robust protection.

Past Performance Record:

- Historical data on customer satisfaction, retention rates, and outcomes achieved for similar clients.

- Testimonials and reviews highlighting successful claim resolutions and cost savings.

Example:

Why Use an RFP for Insurance?

Insurance buying involves long-term financial exposure, regulatory risk, and claims accountability. An RFP insurance creates a controlled way to compare brokers and coverage options using consistent requirements, pricing assumptions, and service standards.

Here’s why insurance teams rely on RFPs:

Secure Coverage That Matches Risk: An RFP forces brokers to price and structure coverage against the same risk profile, limits, and exclusions. This reduces coverage gaps and prevents misaligned proposals.

Create True Market Competition: When multiple brokers or carriers respond to the same requirements, pricing, service models, and claims support can be evaluated side by side, not in isolation.

Validate Compliance and Claims Capability: Insurance RFPs surface a broker’s experience with regulatory obligations, audit readiness, and real claims handling performance, not just policy placement.

Uncover Value Beyond Premiums: RFPs often reveal risk management services, claims advocacy, technology platforms, and employee support programs that are not visible in renewal discussions.

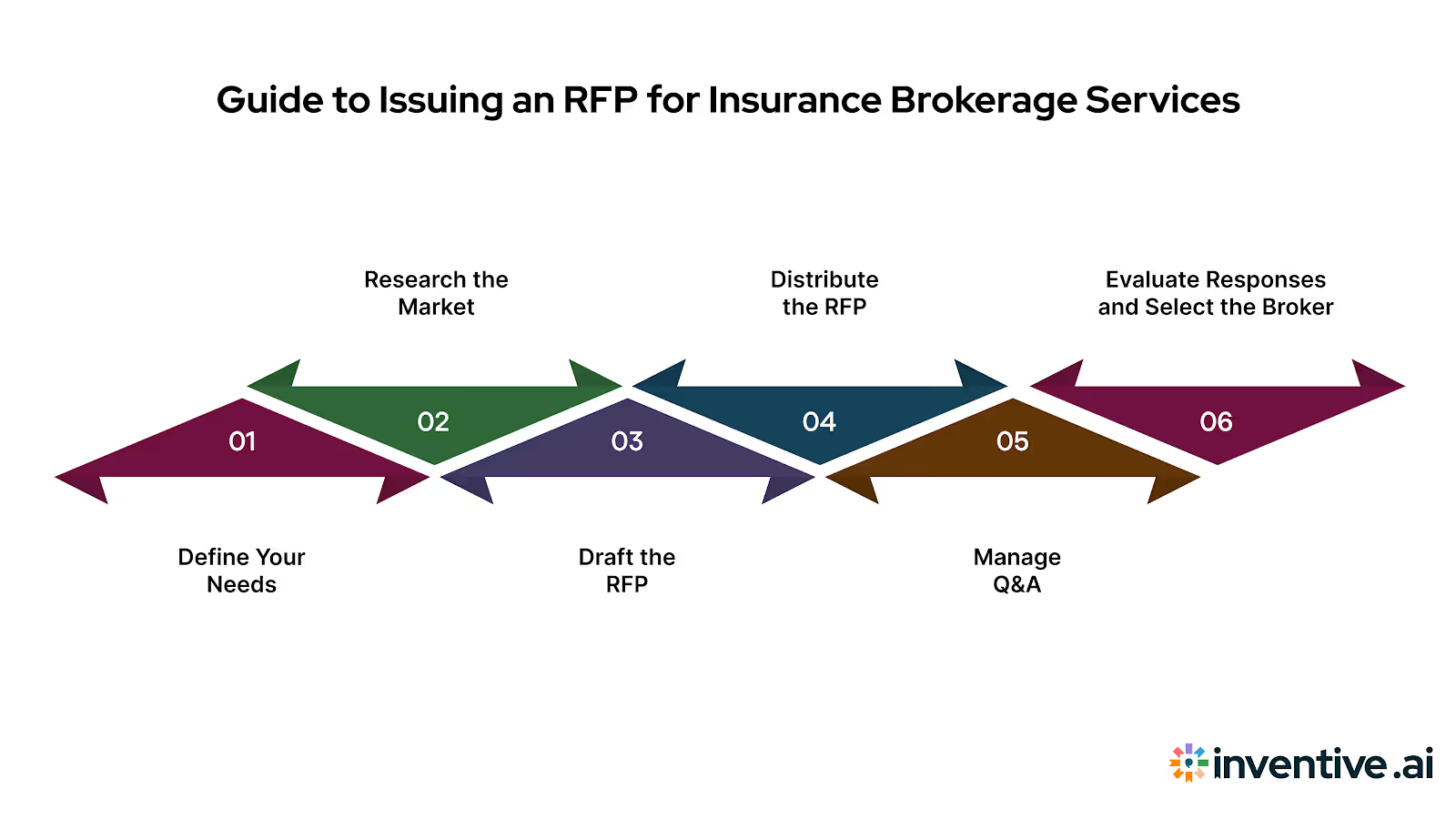

Step-by-Step Guide to Issuing an RFP for Insurance Brokerage Services

Issuing an insurance RFP requires more than drafting a document and collecting responses. The process must control for risk accuracy, pricing consistency, regulatory compliance, and service accountability.

A structured, step-by-step approach ensures brokers are evaluated on the same assumptions, timelines are predictable, and final decisions are defensible across stakeholders.

1. Define Your Needs

Before drafting an RFP, clarify your organization’s insurance requirements. Collaborate with internal stakeholders, including risk management, HR, finance, and legal teams, to identify key priorities.

Example Questions to Consider:

- What types of coverage are needed (e.g., employee benefits, property and casualty)?

- Are there gaps in current coverage that need addressing?

- What value-added services would be beneficial?

Also, define process constraints early, including expected timelines, evaluation ownership, and decision authority. Insurance RFPs often fail when roles and timelines are implied rather than stated.

Typical planning ranges include:

- RFP preparation: 1–2 weeks

- Broker response period: 3–4 weeks

- Evaluation and shortlisting: 2–3 weeks

2. Research the Market

Stay informed about trends in the insurance industry. Look for innovative brokers, emerging technologies, and feedback from peers about their experiences. This research will help you craft a relevant and forward-thinking RFP.

3. Draft the RFP

Use a template as a starting point, but customize it to reflect your organization’s unique needs. Key sections to include:

- Introduction: Provide an overview of your organization and explain the purpose of the RFP.

- Project Scope: Detailed description of the services you’re seeking.

- Requirements: Specific qualifications, certifications, or capabilities needed.

- The timeline includes the deadlines for submission, questions, and selection.

- Submission Guidelines: Instructions for format, page limits, and delivery method.

Sample Question Topics:

- Describe your approach to securing competitive rates.

- Provide examples of compliance support for similar organizations.

- What tools or technology do you offer for collaboration?

4. Distribute the RFP

Decide whether to issue the RFP publicly or to a select group of brokers. While public RFPs cast a wide net, inviting a targeted group of brokers can yield higher-quality responses.

5. Manage Q&A

Anticipate follow-up questions from brokers. Compile all questions, remove duplicates, and distribute answers to maintain transparency and fairness.

6. Evaluate Responses and Select the Broker

Once proposals are received, evaluation should follow a structured scoring model aligned with the criteria defined in the RFP. This prevents decisions based on pricing alone and ensures service, claims capability, and compliance expertise are properly weighted.

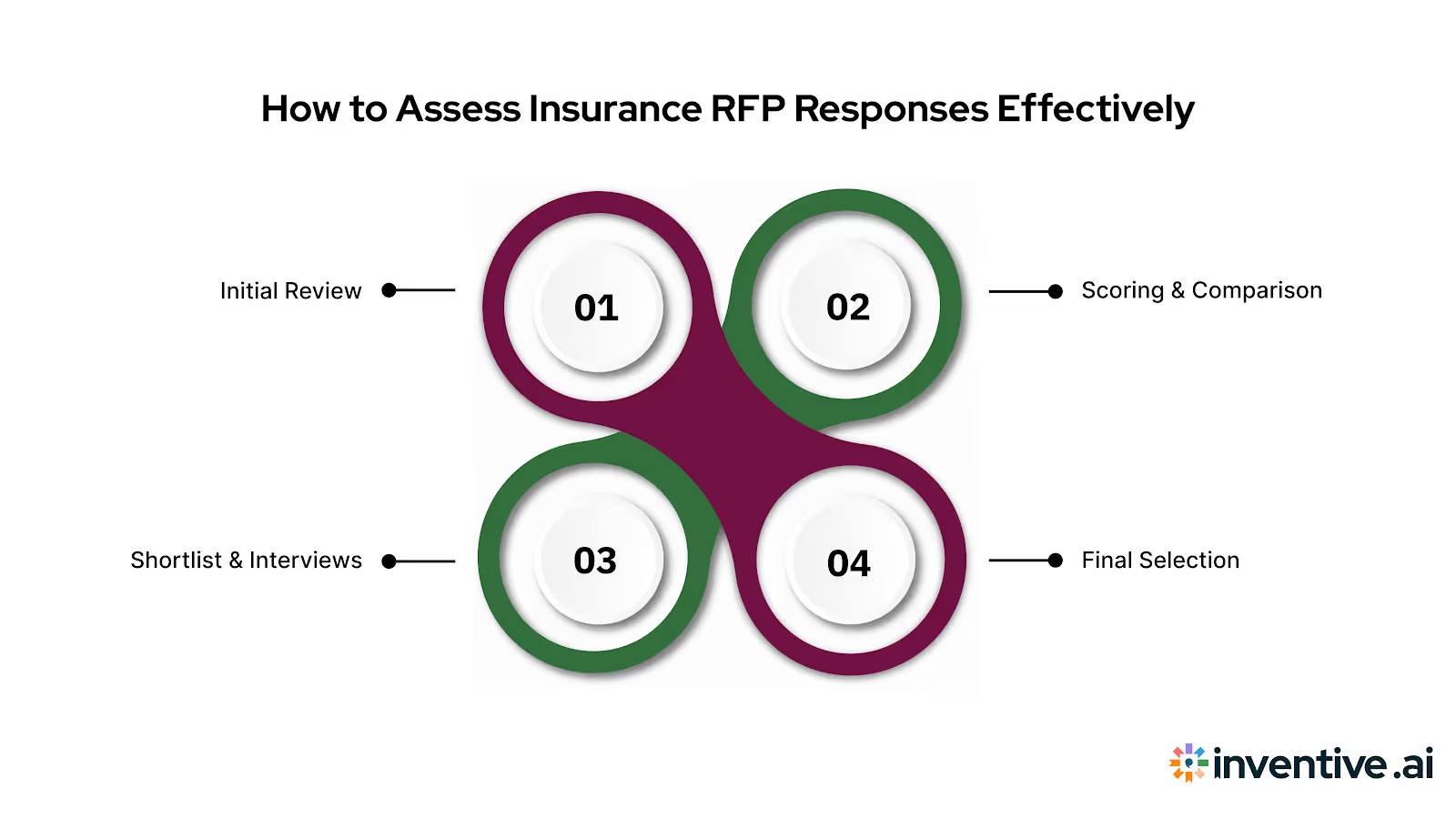

How to Evaluate Insurance RFP Responses Effectively?

Once you’ve received proposals, the evaluation process begins. Here’s how to navigate it:

1. Initial Review

Start by confirming that each proposal meets the minimum requirements outlined in your RFP. Eliminate incomplete or non-compliant responses.

2. Scoring and Comparison

Use a weighted scoring system to objectively evaluate proposals based on predefined criteria. Common evaluation factors include:

- Cost: Does the proposal align with your budget?

- Experience: Has the broker worked with similar organizations?

- Value-Added Services: Are there additional benefits or innovations?

3. Shortlist and Interviews

Narrow down the list to the top candidates. Conduct interviews or request presentations to gain deeper insights into their approach and compatibility with your organization.

4. Final Selection

After careful consideration, select the broker that best meets your needs and aligns with your organizational goals. Notify all participants of your decision and provide constructive feedback to unsuccessful candidates.

Insurance RFP Best Practices: Common Pitfalls and How to Avoid Them

Even well-structured insurance RFPs can underperform when execution gaps appear during planning, distribution, or evaluation. The following best practices address the most common pitfalls and explain how high-performing teams avoid them.

Unclear Evaluation Criteria and Timelines

When brokers are unsure how proposals will be judged or when decisions will be made, responses tend to be generic or misaligned.

Best practice: Clearly document evaluation criteria, scoring weightage, and the full RFP timeline upfront so all respondents price and structure proposals against the same expectations.

Focusing only on the Premium Cost

Lower-priced submissions frequently exclude sub-limits, apply higher deductibles, or shift claims support to third-party administrators. These differences surface only after shortlisting.

Best practice: Evaluate total value by balancing premium, coverage structure, claims handling capability, compliance experience, and ongoing service support.

Rushed Response Windows

Short timelines limit a broker’s ability to conduct market analysis, negotiate with carriers, or model risk accurately.

Best practice: Allow three to four weeks for responses to ensure proposals are well-priced, complete, and comparable.

Generic or Template-Driven RFPs

Templates often fail to capture organization-specific risks, leading to inconsistent assumptions across proposals.

Best practice: Customize each RFP with clear risk details, coverage priorities, and service expectations to eliminate ambiguity.

Poor Documentation and Follow-Through

Undocumented decisions make audits, renewals, and performance reviews difficult.

Best practice: Record communications, evaluation scores, and selection rationale, then define performance metrics to track broker effectiveness after appointment.

When these best practices are applied consistently, insurance RFPs lead to stronger broker partnerships, clearer coverage decisions, and more predictable outcomes over the life of the insurance program.

Why Insurance RFPs Matter for Brokers and Insurance Service Providers?

For insurance brokers and service providers, RFPs act as a formal qualification and positioning mechanism, not just a pricing exercise. The structure of an RFP response directly affects how expertise, coverage approach, claims capability, and service depth are evaluated.

Here’s why RFPs matter for the broker and provider :

- Control How Capabilities Are Evaluated: RFPs provide a defined framework to present coverage strategy, claims support, compliance experience, and service models in a consistent, reviewable format.

- Compete Beyond Premium Comparisons: Well-structured insurance RFPs allow brokers to demonstrate value across risk management, claims handling, regulatory knowledge, and ongoing service, instead of being judged only on price.

- Assess Opportunity Fit Early: RFP requirements make scope, timelines, and expectations explicit, helping teams evaluate alignment before committing significant response effort.

- Demonstrate Industry and Risk Expertise: Questionnaires and evaluation criteria create space to show experience across specific industries, coverage types, and regulatory environments.

- Establish Operational Credibility: Clear, complete RFP responses signal process maturity, transparency, and accountability, influencing shortlisting and final selection decisions.

How to Respond to and Win an Insurance RFP? A Step-by-Step Guide!

For insurance, responding to a Request for Proposal (RFP) is a crucial opportunity to showcase your expertise, align your services with a prospective client’s needs, and secure new business.

To stand out in a competitive field, your proposal must combine strategic positioning, clear differentiation, and a personalized approach.

Here’s a guide tailored specifically for insurance professionals:

1. Evaluate the RFP Opportunity

Before investing time and resources, assess whether the RFP aligns with your firm’s capabilities. Insurance RFPs can vary widely in scope, from employee benefits programs to specialized commercial policies. Consider the following:

- Does your firm have the expertise to address the client’s specific needs?

- Are the lines of coverage or industry segments requested within your core strengths?

- Can you realistically meet the client’s timeline and budget expectations?

By prioritizing opportunities that match your expertise, you can focus on delivering high-quality proposals that maximize your chances of success.

2. Showcase What Sets You Apart

Insurance buyers often evaluate brokers based on the value they bring beyond basic coverage. Clearly articulate your differentiators, tailoring them to the RFP’s requirements.

Key differentiators might include:

- Advanced Technology for Policy Management: Highlight your use of cutting-edge platforms like Inventive.ai, which can streamline policy design, provide actionable analytics, and enhance client communication.

- Claims Management Excellence: Demonstrate your track record of fast and efficient claims resolution. Use metrics like your claims settlement ratio or average payout timelines to establish credibility.

- Tailored Risk Management Solutions: Showcase your ability to design coverage that addresses industry-specific risks, such as cyber threats for tech firms or compliance risks for healthcare organizations.

- Cost Transparency and Competitive Pricing: Assure clients of your commitment to providing clear pricing structures with no hidden fees.

- Industry Expertise: Leverage your track record in the client’s industry to demonstrate a deep understanding of their unique insurance needs.

- Value-Added Services: Mention any additional services you provide, such as wellness programs, loss prevention training, or tools for streamlining the policy renewal process.

These differentiators should be woven into your proposal’s narrative, reinforcing your value proposition at every stage.

3. Personalize the Proposal

A generic proposal won’t resonate in the insurance industry, where each client’s needs are unique. Tailor your submission to the specific priorities mentioned in the RFP.

If the client emphasizes cost control, focus on your ability to deliver competitive pricing and minimize claim costs through proactive risk management. Include case studies or success stories that mirror the client’s situation.

For example:

- Challenge: A mid-sized manufacturing firm needed comprehensive liability coverage while reducing premium costs.

- Solution: Designed a tailored package incorporating advanced risk assessment tools and a self-insured retention program.

- Outcome: Achieved 20% savings on premiums and reduced claim frequency by 15%.

Such examples demonstrate your expertise and instill confidence in your ability to meet the client’s needs.

4. Emphasize Clarity and Structure

Insurance RFP reviewers often assess multiple submissions in a short time. Make your proposal easy to navigate and understand by organizing it clearly. Use concise language and logical sections, such as:

- Executive Summary: A brief overview of your proposal, highlighting your key strengths.

- Coverage Solutions: Detailed descriptions of the policies and services you recommend, tied to the client’s needs.

- Claims and Service Support: Information on claims assistance, customer service, and ongoing support.

- Pricing and Transparency: A clear breakdown of costs and how they compare favorably to competitors.

Leverage tools like Inventive.ai to help refine your content, ensuring it is professionally written, free of errors, and aligned with the client’s expectations.

5. Review and Refine

Errors or inconsistencies can undermine even the strongest proposal. Thoroughly proofread your submission for accuracy, tone, and professionalism. Seek input from colleagues or use AI tools to catch mistakes and polish the final document.

Responding to an insurance RFP is an opportunity to showcase not only your ability to provide coverage but also your commitment to delivering exceptional value and personalized service.

By demonstrating your expertise, differentiators, and client-focused approach while utilizing tools like Inventive.ai to streamline and enhance your proposal, you can position your firm to win more business in the competitive insurance landscape.

How to Respond to an Insurance RFP With Inventive AI?

Inventive AI supports insurance RFP responses by structuring the full response lifecycle, from qualification through submission, using approved insurance content and controlled workflows.

Step 1: Qualify the RFP With a Go or No-Go Assessment

Teams assess scope, coverage lines, timelines, and compliance requirements to determine response fit before committing resources.

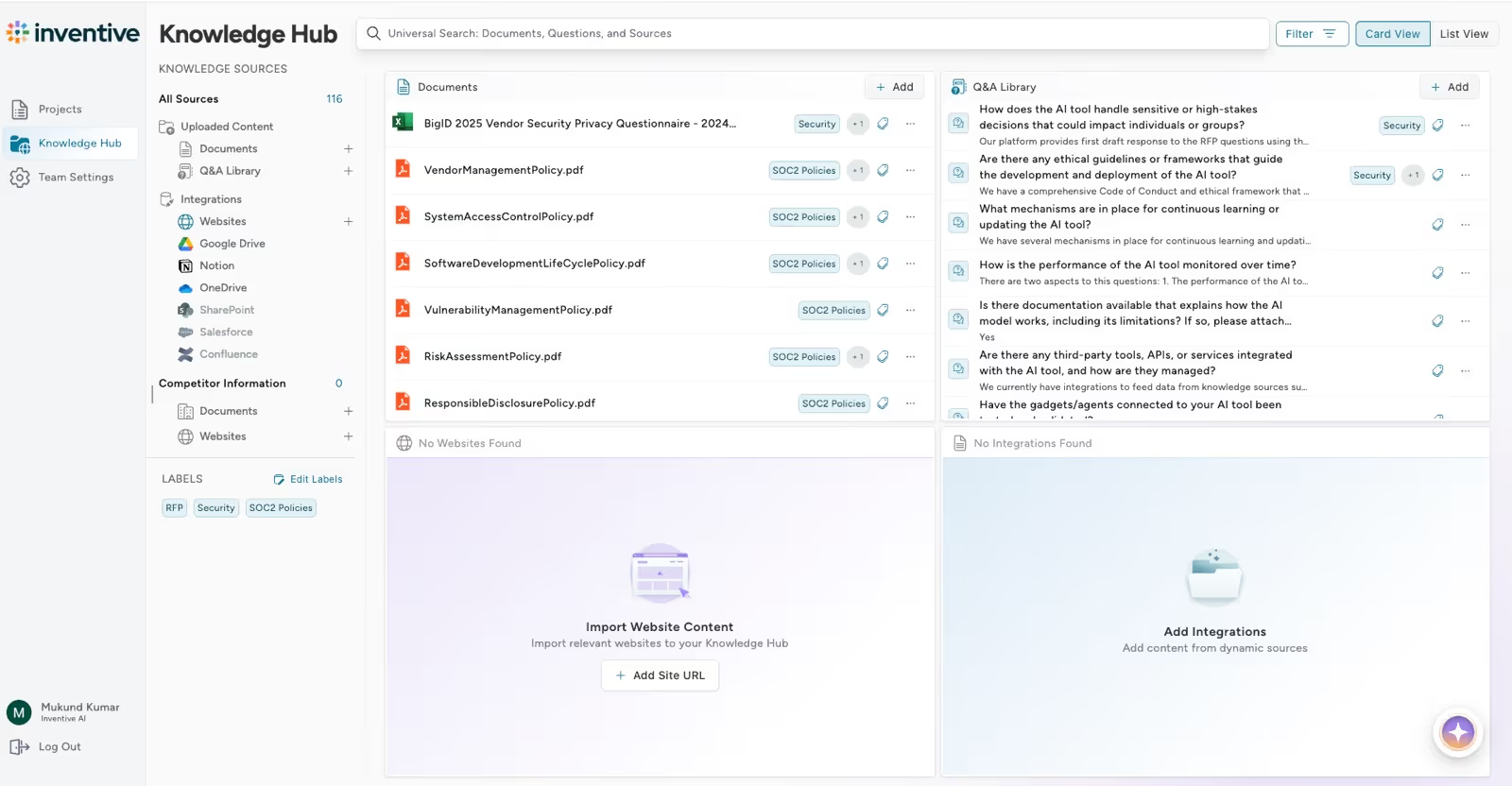

Step 2: Upload and Centralize the Full Insurance RFP Package

All RFP documents, questionnaires, and supporting materials are uploaded into a single workspace to avoid fragmented inputs.

Step 3: Parse Requirements and Map Evaluation Criteria

Inventive AI identifies questions, sections, and evaluation signals to create a structured response framework aligned to buyer expectations.

Step 4: Surface Relevant Insurance-Approved Content

Previously approved insurance responses, policy language, and compliance statements are retrieved and aligned to each requirement.

Step 5: Generate First-Draft Responses Aligned to Insurer Language

Draft responses are generated using consistent insurance terminology and structured to match the buyer’s required format.

Step 6: Review and Validate Responses With Subject Matter Experts

Internal teams review drafts for accuracy, compliance alignment, and risk positioning directly within the response workflow.

Step 7: Refine Differentiation and Risk Positioning

Responses are refined to reflect industry experience, claims capability, and service depth without rewriting entire sections.

Step 8: Lock Structure, Compliance, and Final Formatting

Final checks confirm required disclosures, attachments, and formatting are complete and consistent across the submission.

Step 9: Submit and Capture Learnings for Future RFPs

Final responses and approved language are retained for reuse, improving speed and consistency in future insurance RFPs.

Manual Insurance RFP Responses vs AI Automation

Insurance RFP responses are document-heavy, data-dependent, and repetitive. When handled manually, teams face predictable execution constraints. AI-based RFP automation changes how these constraints are handled at the workflow level.

Respond to Insurance RFPs More Efficiently with Inventive AI

Managing an RFP for insurance is a meticulous but rewarding process. For organizations, it’s the best way to secure optimal coverage and services. For brokers, it’s an opportunity to stand out and win new clients.

By following best practices and leveraging the insights shared in this guide, both sides can achieve their goals and foster successful partnerships.

Whether you’re issuing or responding to an insurance RFP, preparation, clarity, and attention to detail are your greatest allies. With these tools in hand, you’re well-equipped to navigate the RFP process with confidence and success.

Improve how you respond to insurance RFPs with Inventive AI. The platform helps teams generate accurate, structured responses using approved content, reducing manual drafting, formatting effort, and review cycles. This allows responses to stay consistent, complete, and aligned with buyer requirements without increasing operational overhead.

FAQs About Insurance RFPs

1. What is an RFP in insurance?

An insurance RFP is a formal request used by organizations to solicit proposals from insurance brokers or carriers, allowing structured comparison of coverage, pricing, and services.

2. What is an RFP for medical insurance?

A medical insurance RFP focuses on health plans, networks, premiums, wellness programs, compliance requirements, and employee support services.

3. What is RFP in underwriting?

In underwriting, an RFP collects detailed information from carriers about risk assessment methods, pricing logic, exclusions, and claims handling practices.

4. How often should companies run insurance RFPs?

Most organizations conduct insurance RFPs every three to five years, or when major changes in risk exposure, workforce size, or regulatory requirements occur.

5. How long does the insurance RFP process take?

From planning to selection, insurance RFPs typically take six to ten weeks, depending on scope and market complexity.

90% Faster RFPs. 50% More Wins. Watch a 2-Minute Demo.

Dhiren Bhatia

Dhiren Bhatia has spent over 20 years in enterprise tech solving one problem: RFPs take too long and cost too much. As CEO of Viewics, a healthcare analytics company he founded and sold to Roche, he led teams through countless RFP cycles and saw firsthand how much time manual work wasted. That experience led him to start Inventive AI, where he's now Co-founder and CEO, building AI that helps RFP teams cut response time by up to 90% and win more deals.

.avif)

Mukund Kumar

Mukund Kumar is Growth Marketing Manager at Inventive AI. An IIT Jodhpur graduate with 3+ years in growth and performance marketing, he specializes in data-driven strategies that connect sales and RFP teams with the automation they actually need, helping revenue teams cut through generic AI hype and win more deals.